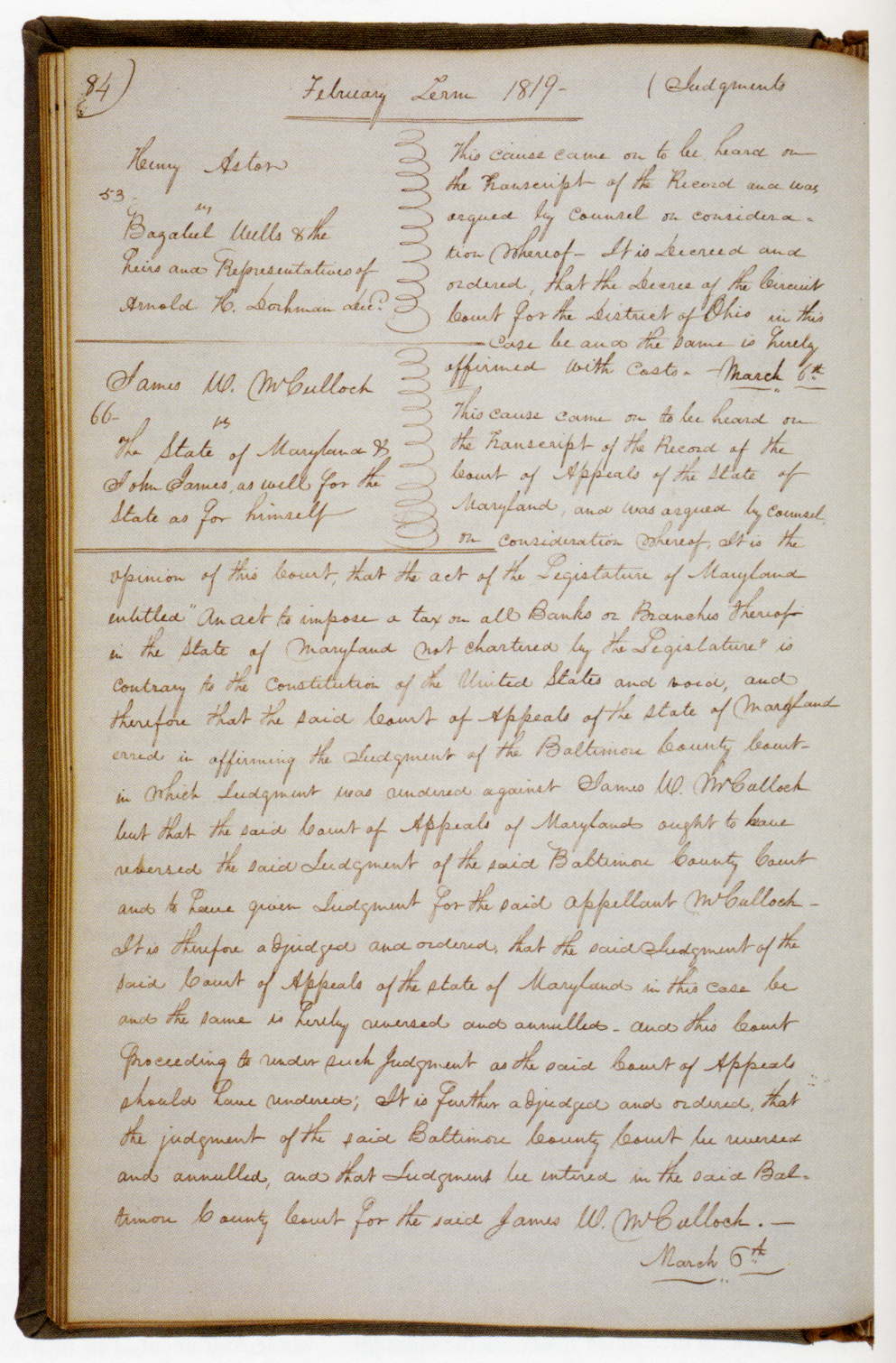

McCulloch

vs. Maryland |

In 1816 Congress established the Second National Bank to help control the amount of unregulated currency issued by state banks. Many states questioned the constitutionality of the national hank, and Maryland set a precedent by requiring taxes from all hanks that the state had not chartered. In 1818 the State of Maryland approved legislation to impose taxes on the Second National Bank, because Congress had chartered it. James W. McCulloch, a cashier at the Baltimore branch of the U.S. bank, refused to pay the taxes the state was demanding. In response, Maryland filed a suit against McCulloch. McCulloch v. Maryland became a major challenge to the Constitution: Does the federal government hold sovereign power over states? The proceedings added two questions: Does the Constitution empower Congress to create a bank? And could individual states ban or tax the bank? The court decided that the federal government had the right and power to set up a federal bank and that states did not have the power to tax the federal government. Chief Justice John Marshall ruled in favor of the federal government and concluded, "The power to tax involves the power to destroy." In this landmark Supreme Court case, Chief Justice Marshall handed down one of his most important decisions regarding the expansion of federal power. McCulloch v. Maryland is one of the foundations of the division of powers between state and federal governments.

CHIEF JUSTICE MARSHALL DELIVERED THE OPINION OF THE COURT. In the case now to be determined, the defendant, a sovereign State, denies the obligation of a law enacted by the legislature of the Union, and the plaintiff, on his part, contests the validity of an act which has been passed by the legislature of that State. The constitution of our country, in its most interesting and vital parts, is to be considered; the conflicting powers of the govern- ment of the Union and of its members, as marked in that constitution, are to be discussed; and an opinion given, which may essentially influence the great operations of the government. No tribunal can approach such a question without a deep sense of its importance, and of the awful responsibility involved in its decision! But it must be decided peacefully, or remain a source of hostile legislation, perhaps of hostility of a still more serious nature; and if it is to be so decided, by this tribunal alone can the decision be made. On the Supreme Court of the United States has the constitution of our country devolved this important duty. The first question made in the cause is, has Congress power to incorporate a bank?

This government is acknowledged by all to be one of enumerated powers. The principle, that it can exercise only the powers granted to it, [is] now universally admitted. But the question respecting the extent of the powers actually granted, is perpetually arising, and will probably continue to arise, as long as our system shall exist.

Among the enumerated powers, we do not find that of establishing a bank or creating a corporation. But there is no phrase in the instrument which, like the articles of confederation, excludes incidental or implied powers; and which requires that everything granted shall be expressly and minutely described. Even the 10th amendment, which was framed for the purpose of quieting the excessive jealousies which had been excited, omits the word "expressly," and declares only that the powers "not delegated to the United States, nor prohibited to the States, are reserved to the States or to the people"; thus leaving the question, whether the particular power which may become the subject of contest has been delegated to the one government, or prohibited to the other, to depend on a fair construction of the whole instrument. The men who drew and adopted this amendment had experienced the embarrassments resulting from the insertion of this word in the articles of confederation, and probably omitted it to avoid those embarrassments. A constitution, to contain an accurate detail of all the subdivisions of which its great powers will admit, and of all the means by which they may be carried into execution, would partake of the prolixity of a legal code, and could scarcely be embraced by the human mind. It would probably never be understood by the public. Its nature, therefore, requires, that only its great outlines should be marked, its important objects designated, and the minor ingredients which compose those objects be deduced from the nature of the objects themselves....

After the most deliberate consideration, it is the unanimous and decided opinion of this Court, that the act to incorporate the Bank of the United States is a law made in pursuance of the constitution, and is a part of the supreme law of the land....

[W]e proceed to inquire—

2. Whether the State of Maryland may, without violating the constitution, tax that branch?

That the power of taxation is one of vital importance; that it is retained by the States; that it is not abridged by the grant of a similar power to the government of the Union; that it is to be concurrently exercised by the two governments: are truths which have never been denied. But, such is the paramount character of the constitution, that its capacity to withdraw any subject from the action of even this power, is admitted. The States are expressly forbidden to lay any duties on imports or exports, except what may be absolutely necessary for executing their inspection laws. If the obligation of this prohibition must be conceded, the same paramount character would seem to restrain, as it certainly may restrain, a State from such other exercise of this power; as is in its nature incompatible with, and repugnant to, the constitutional laws of the Union....

On this ground the counsel for the bank place its claim to be exempted from the power of a State to tax its operations. There is no express provision for the case, but the claim has been sustained on a principle which so entirely pervades the constitution, is so intermixed with the materials which compose it, so interwoven with its web, so blended with its texture, as to be incapable of being separated from it, without rending it into shreds.

This great principle is, that the constitution and the laws made in pursuance thereof are supreme; that they control the constitution and laws of the respective States, and cannot be controlled by them. From this, which may be almost termed an axiom, other propositions are deduced as corollaries, on the truth or error of which, and on their application to this case, the cause has been supposed to depend. These are, 1ST. that a power to create implies a power to preserve. 2ND. That a power to destroy, if wielded by a different hand, is hostile to, and incompatible with these powers to create and to preserve. 30. That where this repugnancy exists, that authority which is supreme must control, not yield to that over which it is supreme....

That the power of taxing by the States may be exercised so as to destroy it, is too obvious to be denied. But taxation is said to be an absolute power, which acknowledges no other limits than those expressly prescribed in the constitution, and like sovereign power of every other description, is trusted to the discretion of those who use it. But the very terms of this argument admit that the sovereignty of the State, in the article of taxation itself, is subordinate to, and may be controlled by, the constitution of the United States....

In the legislature of the Union alone, are all represented. The legislature of the Union alone, therefore, can be trusted by the people with the power of control- ling measures which concern all, in the confidence that it will not be abused....

If we apply the principle for which the State of Maryland contends, to the constitution generally, we shall find it capable of changing totally the character of that instrument. We shall find it capable of arresting all the measures of the government, and of prostrating it at the foot of the States. The American people have declared their constitution, and the laws made in pursuance thereof, to be supreme; but this principle would transfer the supremacy, in fact, to the States....

The Court has bestowed on this subject its most deliberate consideration. The result is a conviction that the States have no power, by taxation or otherwise, to retard, impede, burden, or in any manner control, the operations of the constitutional laws enacted by Congress to carry into execution the powers vested in the general government. This is, we think, the unavoidable consequence of that supremacy which the constitution has declared.

We are unanimously of opinion, that the law passed by the legislature of Maryland, imposing a tax on the Bank of the United States, is unconstitutional and void....