At first the huge investment bank Bear Stearns was in deep

trouble. JP Morgan (supported by a $30

billion federal loan) agreed to buy out Bear Sterns, thus avoiding a

catastrophe, and calming down the nervous stock market (for a while anyway).

Then by the summer of 2008, America's biggest mortgage companies, the Federal

National Mortgage Association (Fannie Mae) and the Federal Home Loan

Mortgage Corporation (Freddie Mac)[1]

were on the edge of bankruptcy. Here too

the federal government stepped in to offer $100 billion to get these two

companies going again. Then in September

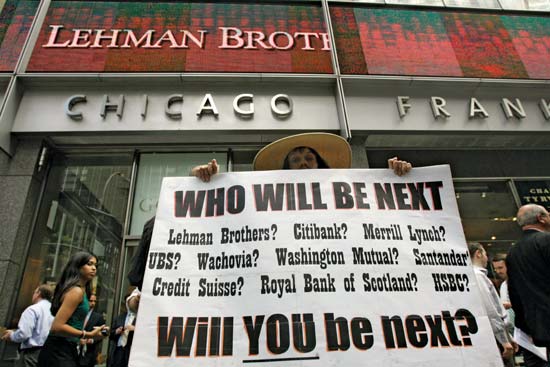

Lehman Brothers was in similar trouble.

But no purchaser could be found to buy out the company, even at a

greatly reduced rate. Bankruptcy

resulted. Likewise, the stock brokerage

company Merrill Lynch and the huge banking company Washington Mutual

collapsed. Then the Federal Reserve

itself stepped in to bail out ($180 billion) the massive insurance company,

American International Group, when the AIG found itself facing bankruptcy.

A protest in front of the Lehman

Brothers headquarters in New York

A protest in front of the Lehman

Brothers headquarters in New York Lehman Brothers CEO

Richard Fuld heckled by protesters

Lehman Brothers CEO

Richard Fuld heckled by protesters

upon leaving Capitol Hill – October

2008

But

the Republicans were ready to let the companies fall into bankruptcy (and

restructuring); the Democrats however wanted to save the companies – and thus

the jobs of all the workers whose support they depended on politically.

But

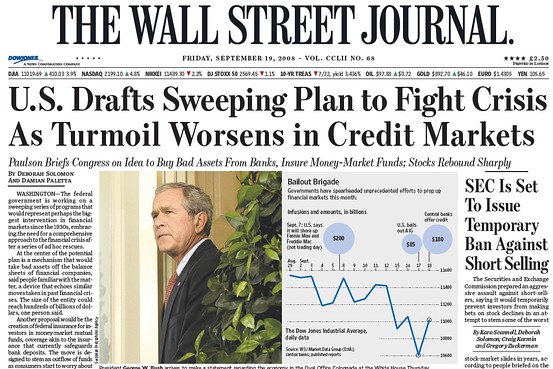

by this time the stock market was finally in full panic mode. Bush then stepped into the picture in

late September, presenting to Congress a request in the form of a $700 billion

Troubled Assets Relief Program (TARP), to extend federal loans to

troubled companies. The Republicans at first balked at this "socialist"

idea. But when in response to this "no"

the very next day the Dow Jones Stock Market index lost 778 points (the worst

single-day drop in the history of the stock market), the Republicans were

forced to back down and accept TARP.

September 29, 2008 – Treasury

Secretary Hank Paulson (with

Federal Reserve chief Bernanke at his side) begs Congress

to authorize the

$700 billion corporate bail-out package (the

"Paulson Plan"). Congress's first answer

was a "no" ... which

immediately plunged the Dow 778

points – the worst single-

day loss in the history of the New York's Wall Street stock

market (at that point).

But

it was not just the housing industry that was behind this crisis. The same was happening in the automobile

industry. The "Big Three"

Detroit auto manufacturers (Ford, General Motors and Chrysler)

were also having big problems selling their cars. Gas prices were running at a high of $4 a

gallon, causing a drop in the sales of Detroit's best-selling SUV and pickup

trucks (the big money-makers for Detroit).

Where there was still any action in the automobile sector it was in the

realm of the small sedans – where German and Japanese companies were actually

doing quite well, especially with the models manufactured in America by a

younger workforce (lower salaries and less expensive health and pension

benefits required). These foreign

companies had over the previous ten years increased their percentage of overall

car sales from 30% to 47%. Detroit was

falling into deep trouble. And thus it

was (again despite Republican resistance) $17 billion of the TARP funds were directed to helping

Detroit – with the proviso that the unions would be willing to accept cutbacks

on their wages and benefits.

And then Bush left the office as American president. It would be somebody else's job to steer the

country through what remained of this economic mess.

[1]Despite the names, these are not federally-owned or federally-operated

mortgage companies, only federally-originated – but definitely privately-run

banks, operating like any other mortgage bank.

Go on to the next section:

Miles

H. Hodges

Miles

H. Hodges

The "easy money" disaster

The "easy money" disaster

Market saturation bursts the speculative bubble

Market saturation bursts the speculative bubble  Panic sets in (2008)

Panic sets in (2008)